All Categories

Featured

Table of Contents

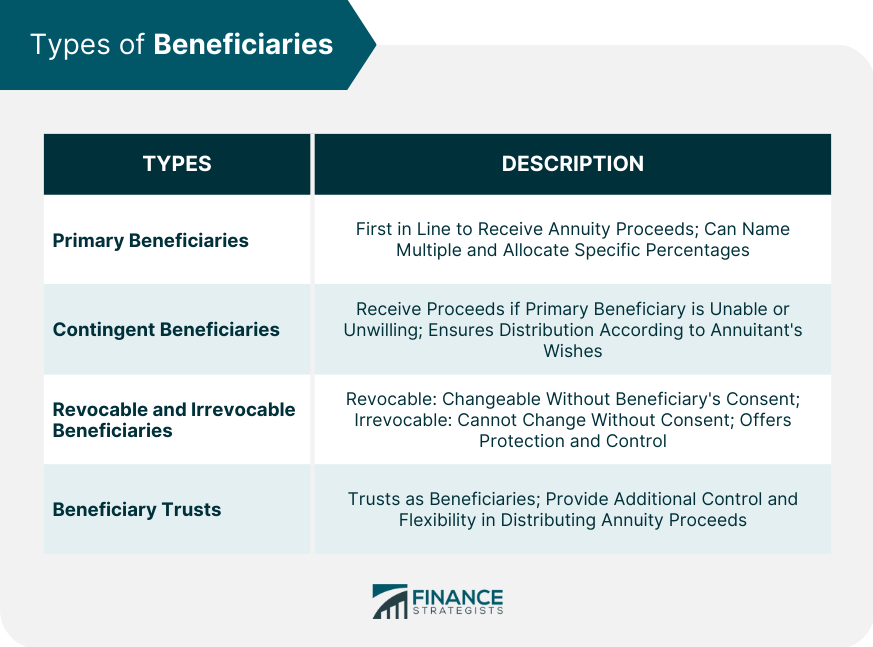

Maintaining your classifications up to day can make sure that your annuity will be taken care of according to your desires need to you pass away unexpectedly. Besides an annual evaluation, significant life occasions can motivate annuity proprietors to rethink at their recipient options. "A person may want to upgrade the recipient classification on their annuity if their life circumstances change, such as marrying or separated, having kids, or experiencing a fatality in the family," Mark Stewart, Certified Public Accountant at Action By Action Organization, informed To change your beneficiary designation, you must connect to the broker or representative who handles your contract or the annuity company itself.

Similar to any kind of monetary item, seeking the assistance of a financial advisor can be valuable. A monetary coordinator can lead you with annuity monitoring processes, including the approaches for updating your contract's recipient. If no beneficiary is named, the payment of an annuity's survivor benefit mosts likely to the estate of the annuity owner.

Acquiring an annuity can be a fantastic windfall, yet can additionally increase unanticipated tax obligations and administrative problems to handle. In this article we cover a few fundamentals to be knowledgeable about when you acquire an annuity. Initially, know that there are 2 kinds on annuities from a tax perspective: Qualified, or non-qualified.

When you take money out of an inherited qualified annuity, the total withdrawn will certainly be counted as taxed earnings and strained at your ordinary revenue tax obligation rate, which can be rather high relying on your monetary scenario. Non-qualified annuities were moneyed with cost savings that already had actually taxes paid. You will not owe tax obligations on the initial expense basis (the overall payments made at first right into the annuity), but you will still owe tax obligations on the development of the financial investments however and that will certainly still be exhausted as revenue to you.

Specifically if the initial annuity owner had been receiving repayments from the insurance business. Annuities are usually made to supply earnings for the original annuity proprietor, and afterwards cease settlements as soon as the original proprietor, and possibly their spouse, have actually passed. There are a couple of circumstances where an annuity might leave an advantage for the beneficiary inheriting the annuity: This suggests that the preliminary owner of the annuity was not receiving normal payments from the annuity.

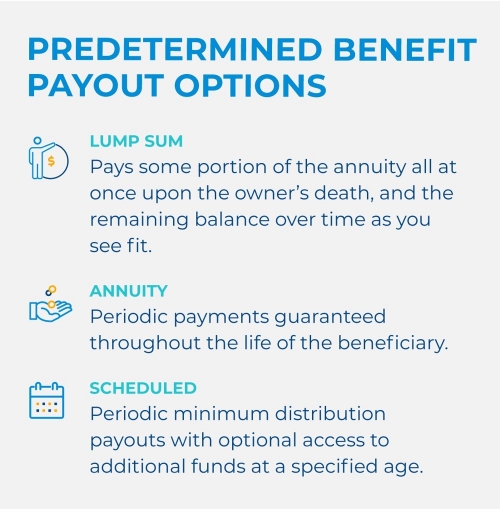

The beneficiaries will have several choices for how to get their payment: They might keep the money in the annuity, and have the properties transferred to an inherited annuity account (Annuity income stream). In this case the assets may still continue to be invested and remain to expand, nevertheless there will be called for withdrawal rules to be aware of

Tax treatment of inherited Single Premium Annuities

You might likewise be able to pay out and receive a lump sum settlement from the inherited annuity. Be sure you recognize the tax impacts of this decision, or talk with a monetary advisor, because you may be subject to considerable earnings tax obligation by making this political election. If you elect a lump-sum payout alternative on a qualified annuity, you will based on revenue taxes on the entire value of the annuity.

Another feature that may exist for annuities is a guaranteed fatality benefit (Flexible premium annuities). If the initial owner of the annuity chosen this attribute, the beneficiary will certainly be qualified for an one-time round figure advantage. Exactly how this is strained will certainly rely on the sort of annuity and the value of the death benefit

The particular policies you should follow rely on your partnership to the individual that passed away, the kind of annuity, and the phrasing in the annuity contract sometimes of purchase. You will certainly have a set amount of time that you have to withdrawal the assets from the annuity after the preliminary owners fatality.

As a result of the tax obligation effects of withdrawals from annuities, this indicates you require to carefully intend on the ideal method to withdraw from the account with the most affordable amount in tax obligations paid. Taking a big round figure might press you right into extremely high tax braces and lead to a larger section of your inheritance mosting likely to pay the tax bill.

It is likewise important to know that annuities can be exchanged. This is recognized as a 1035 exchange and allows you to move the cash from a certified or non-qualified annuity right into a various annuity with another insurance coverage company. This can be a good alternative if the annuity agreement you acquired has high charges, or is simply not right for you.

Taking care of and spending an inheritance is extremely important duty that you will be pushed into at the time of inheritance. That can leave you with a great deal of questions, and a great deal of prospective to make expensive mistakes. We are here to assist. Arnold and Mote Riches Monitoring is a fiduciary, fee-only financial coordinator.

Do you pay taxes on inherited Structured Annuities

Annuities are just one of the several tools financiers have for developing wide range and safeguarding their monetary well-being. An inherited annuity can do the very same for you as a beneficiary. are contracts between the insurer that release them and individuals who purchase them. There are different kinds of annuities, each with its own advantages and functions, the key facet of an annuity is that it pays either a series of settlements or a swelling sum according to the agreement terms.

If you lately inherited an annuity, you might not know where to begin. Annuity proprietor: The person who enters right into and pays for the annuity contract is the proprietor.

An annuity might have co-owners, which is frequently the case with partners. The proprietor and annuitant might be the same individual, such as when a person purchases an annuity (as the owner) to provide them with a repayment stream for their (the annuitant's) life.

Annuities with numerous annuitants are called joint-life annuities. As with multiple owners, joint-life annuities are a typical framework with pairs due to the fact that the annuity proceeds to pay the making it through spouse after the very first spouse passes.

It's feasible you may obtain a survivor benefit as a recipient. That's not always the case. When a survivor benefit is triggered, payments may depend in component on whether the owner had currently started to receive annuity settlements. An acquired annuity death benefit works differently if the annuitant had not been currently obtaining annuity repayments at the time of their death.

When the advantage is paid to you as a swelling amount, you receive the entire amount in a single payout. If you choose to receive a settlement stream, you will certainly have numerous alternatives offered, depending on the agreement. If the owner was currently getting annuity repayments at the time of fatality, then the annuity contract may just terminate.

{kind=link}

Table of Contents

Latest Posts

Exploring the Basics of Retirement Options A Closer Look at How Retirement Planning Works What Is Fixed Vs Variable Annuity? Pros and Cons of Various Financial Options Why Choosing the Right Financial

Breaking Down Your Investment Choices A Closer Look at How Retirement Planning Works Breaking Down the Basics of Fixed Interest Annuity Vs Variable Investment Annuity Pros and Cons of Various Financia

Decoding How Investment Plans Work A Comprehensive Guide to Investment Choices What Is Fixed Annuity Or Variable Annuity? Features of Smart Investment Choices Why What Is A Variable Annuity Vs A Fixed

More

Latest Posts